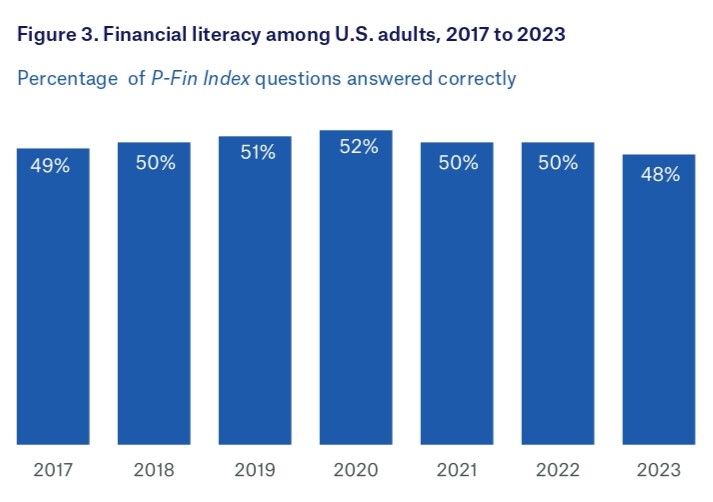

The widely used TIAA Institute-GFLEC Personal Finance Index (P-Fin Index) is an annual barometer of knowledge and understanding on personal finances. The index is based on 28 questions. On average, only 50% of these 28 questions are answered correctly. This is a failing grade! Financial illiteracy is, unfortunately, holding steady as seen by the below chart.